Cost of capital formula

/What is the Cost of Capital Formula?

The cost of capital formula is the blended cost of debt and equity that a company has acquired in order to fund its operations. It is important, because a company’s investment decisions related to new operations should always result in a return that exceeds its cost of capital – if not, then the company is not generating a return for its investors.

How to Calculate the Cost of Capital

The cost of capital is comprised of the costs of debt, preferred stock, and common stock. The formula for the cost of capital is comprised of separate calculations for all three of these items, which must then be combined to derive the total cost of capital on a weighted average basis. To derive the cost of debt, multiply the interest expense associated with the debt by the inverse of the tax rate percentage, and divide the result by the amount of debt outstanding. The amount of debt outstanding that is used in the denominator should include any transactional fees associated with the acquisition of the debt, as well as any premiums or discounts on sale of the debt. These fees, premiums, or discounts should be gradually amortized over the life of the debt, so that the amount included in the denominator will decrease over time. The formula for the cost of debt is as follows:

(Interest Expense x (1 – Tax Rate) ÷

Amount of Debt – Debt Acquisition Fees + Premium on Debt – Discount on Debt

Related AccountingTools Courses

The cost of preferred stock is a simpler calculation, since interest payments made on this form of funding are not tax-deductible. The formula is as follows:

Interest Expense ÷ Amount of Preferred Stock

The calculation of the cost of common stock requires a different type of calculation. It is composed of three types of return: a risk-free return, an average rate of return to be expected from a typical broad-based group of stocks, and a differential return that is based on the risk of the specific stock in comparison to the larger group of stocks. The risk-free rate of return is derived from the return on a U.S. government security. The average rate of return can be derived from any large cluster of stocks, such as the Standard & Poor’s 500 or the Dow Jones Industrials. The return related to risk is called a stock’s beta; it is regularly calculated and published by several investment services for publicly-held companies, such as Value Line. A beta value of less than one indicates a level of rate-of-return risk that is lower than average, while a beta greater than one would indicate an increasing degree of risk in the rate of return. Given these components, the formula for the cost of common stock is as follows:

Risk-Free Return + (Beta x (Average Stock Return – Risk-Free Return))

Once all of these calculations have been made, they must be combined on a weighted average basis to derive the blended cost of capital for a company. We do this by multiplying the cost of each item by the amount of outstanding funding associated with it, as noted in the following table:

|

Total Debt Funding |

x |

Percentage Cost |

= |

Dollar Cost of Debt |

|

Total Preferred Stock Funding |

x |

Percentage Cost |

= |

Dollar Cost of Preferred Stock |

|

Total Common Funding |

x |

Percentage Cost |

= |

Dollar Cost of Common Stock |

|

= |

Total Cost of Capital |

Example of the Cost of Capital

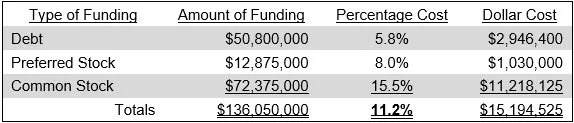

An investment analyst wants to determine the cost of capital of the Jolt Electric Company, to see if it is generating returns that exceed its cost of capital. The return it reported for its last fiscal year was 11.8%. The company’s bonds are currently priced on the open market at a total price of $50,800,000, its preferred stock at $12,875,000, and its common stock at $72,375,000. Its incremental tax rate is 34%. It pays $4,625,000 in interest on its bonds, and there is an unamortized debt premium of $1,750,000 currently on the company’s books. The preferred stock pays interest of $1,030,000. The risk-free rate of return is 5%, the return on the Dow Jones Industrials is 12%, and Jolt’s beta is 1.5. To calculate Jolt’s cost of capital, we first determine its cost of debt, which is as follows:

($4,625,000 Interest Expense) x (1 - .34 Tax Rate)

----------------------------------------------------------------

$50,800,000 Debt + $1,750,000 Unamortized Premium

= 5.8%

The investment analyst then proceeds to the cost of preferred stock, which is calculated as follows:

$1,030,000 Interest Expense

------------------------------------

$12,875,000 Preferred Stock

= 8.0%

Finally, the analyst calculates the cost of common stock, which is as follows:

5% Risk-Free Return + (1.5 Beta x (12% Average Return – 5% Risk-Free Return) = 15.5%

The analyst then creates the following weighted-average table to determine the combined cost of capital for Jolt:

Based on these calculations, Jolt’s return of 11.8% is a marginal improvement over its cost of capital of 11.2%.

Advantages of the Cost of Capital

There are multiple advantages to using the cost of capital. First, it serves as a threshold value for whether a project will be accepted or not. Second, it sets a minimum value for investments that ensures a positive rate of return on funds, which increases the value of the firm from the perspective of investors. Third, it provides a threshold value that must be met for prospective acquisitions; if there is no way to achieve a return from an acquisition that at least matches the cost of capital, then the acquirer will lose value if it completes the acquisition.

Issues with the Cost of Capital

The dollar value of the preferred stock and common stock used in this calculation is based on the current market price of these items, rather than the price at which they were originally sold. By using the market rate, you can more accurately determine the assumed rate of return that investors are expecting at the moment; this is much preferable to using the book rate for either item, since this fixes the rate of return at the time when the shares were originally sold, and gives no indication of current market expectations.

FAQs

What is the difference between the cost of capital and the discount rate?

The cost of capital is the company’s required return on the funds it raises from debt and equity holders, reflecting its overall financing cost, often expressed as the weighted average cost of capital. The discount rate is the rate used in a specific valuation or capital budgeting analysis to convert future cash flows into present value. While the discount rate is often based on the cost of capital, it may be adjusted upward or downward to reflect project-specific risk, financing structure, or strategic considerations.

What is the difference between the cost of capital and the cost of equity?

The cost of capital is the overall required return that a company must earn to satisfy all providers of capital, including both debt and equity holders, typically measured as the weighted average cost of capital. The cost of equity is the specific return required by shareholders for investing in the company’s common stock, reflecting the risk of ownership without contractual repayment. The cost of equity is therefore one component of the broader cost of capital calculation.