Variable costing income statement definition

/What is a Variable Costing Income Statement?

A variable costing income statement is one in which all variable expenses are deducted from revenue to arrive at a separately-stated contribution margin, from which all fixed expenses are then subtracted to arrive at the net profit or loss for the period. This presentation format is rarely used, since most organizations prefer a format that combines variable and fixed costs within a cost of goods sold section, after which all remaining expenses are subtracted from the gross margin.

When to Use a Variable Costing Income Statement

There are a few highly specific situations in which it can make sense to construct a variable costing income statement. They are as follows:

For determining expense variability. It is useful to create an income statement in the variable costing format when you want to determine that proportion of expenses that truly varies directly with revenue. In many businesses, the contribution margin will be substantially higher than the gross margin, because such a large amount of its production costs are fixed, and very few of its selling and administrative expenses are variable.

For product-level reporting. This statement structure is especially useful when it is prepared at the level of an individual product or product line, so that you can see if the products are generating a positive return. Stripping away the fixed costs from the top of this reporting format makes the product contribution margin much more obvious. In addition, this reporting format will reveal which products need either a price increase or a cost reduction in order to generate an acceptable contribution margin.

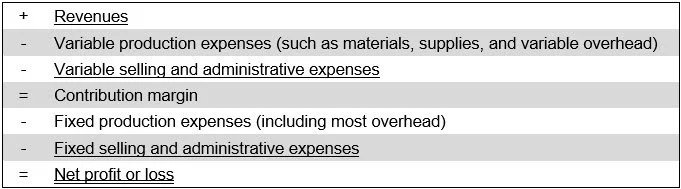

The Structure of a Variable Costing Income Statement

A variable income statement varies from a normal income statement in three respects. First, all fixed production costs are aggregated lower in the statement, after the contribution margin. Second, all variable selling and administrative expenses are grouped with variable production costs, so that they are a part of the calculation of the contribution margin. And finally, the gross margin is replaced by the contribution margin. Thus, the format of a variable costing income statement is:

In many cases, direct labor should be categorized as a fixed expense in this income statement format, rather than a variable expense, because this cost does not usually change in direct proportion to the amount of revenue generated. Instead, management needs to keep a certain number of employees in the production area within a certain production volume range.

The key difference between gross margin and contribution margin is that fixed production costs are included in the cost of goods sold to arrive at the gross margin, whereas fixed production costs are not included in the same calculation for the contribution margin. This means that the variable costing income statement is sorted based on the variability of the underlying cost information, rather than by the functional areas or expense categories that are found in a more typical income statement.

Under both the variable costing income statement and a normal income statement, the net profit or loss will be the same.

Related Articles

Contribution Margin Income Statement