Capital budgeting definition

/What is Capital Budgeting?

Capital budgeting is the process that a business uses to determine which proposed fixed asset purchases it should accept, and which should be declined. This process is used to create a quantitative view of each proposed fixed asset investment, thereby giving a rational basis for making a judgment. This analysis is especially necessary when there are not enough funds available to pay for all of the projects being requested. Lenders may require this analysis when they are being asked to loan funds to pay for a project; they can then review the analysis to gain a better understanding of the cash flows involved, as well as the risks of failure.

Capital Budgeting Methods

There are a number of methods commonly used to evaluate fixed assets under a formal capital budgeting system. The more important ones are noted below.

Net Present Value Analysis

Under net present value analysis, identify the net change in cash flows associated with a fixed asset purchase, and discount them to their present value. Then compare all proposed projects with positive net present values, and accept those with the highest net present values until funds run out. A concern with using net present value analysis is that the future cash flows associated with a project are uncertain, and are subject to manipulation. The result can be projected cash flows that have been adjusted to ensure that a project will be approved. This issue can only be discovered after the fact, by comparing actual to projected cash flows. Another concern with net present value analysis is that the discount rate used to derive present values can be adjusted downward to ensure that a project is approved; this is usually justified on the grounds that a project is low risk. In short, this supposedly quantitative analysis method is actually subject to qualitative alterations that can significantly impact the decision outcome.

Constraint Analysis

Under constraint analysis, identify the bottleneck machine or work center in a production environment and invest in those fixed assets that maximize the utilization of the bottleneck operation. Under this approach, a business is less likely to invest in areas downstream from the bottleneck operation (since they are constrained by the bottleneck operation) and more likely to invest upstream from the bottleneck (since additional capacity there makes it easier to keep the bottleneck fully supplied with inventory). This is perhaps the best capital budgeting analysis tool, since it can consistently result in capital investments that improve company profits.

Payback Period

Under the payback approach, determine the period required to generate sufficient cash flow from a project to pay for the initial investment in it. This is essentially a risk measure, for the focus is on the period of time that the investment is at risk of not being returned to the company. This analysis is most useful when used as a supplement to the preceding two analysis methods, rather than as the primary basis for deciding whether to make an investment.

Avoidance Analysis

Under avoidance analysis, determine whether increased maintenance can be used to prolong the life of existing assets, rather than investing in replacement assets. This analysis can substantially reduce a company's total investment in fixed assets. This is an especially useful option when the incremental maintenance expenditure is not significant, such as when there is no need for a major equipment overhaul. However, it may make more sense to upgrade to new equipment when the skills required to maintain the current equipment are so difficult to obtain that the business would be in trouble if its maintenance personnel were to leave the company.

Related AccountingTools Courses

Capital Budgeting Forms

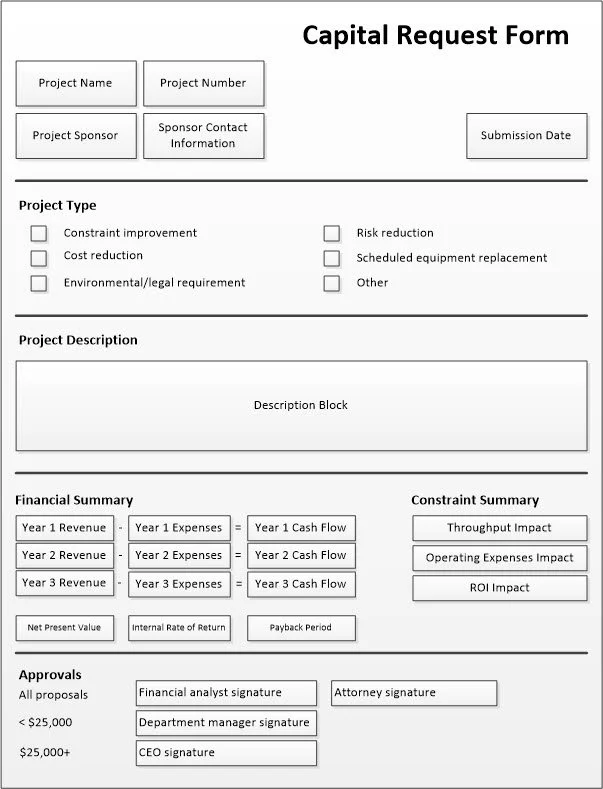

A business will usually institute a formal procedure for capital budgeting, in order to provide a consistent flow of information to those tasked with making investment decisions. Part of this procedure will likely be a standardized capital budgeting request form, in which the applicant states the case of investing in a particular project. An example appears below, containing separate blocks that identify a project, state the type of project, describe it, and provide a summary of its financial and constraint impacts. There is also a signature block at the bottom, to be filled out by those authorized to do so.

The Importance of Capital Budgeting

The amount of cash involved in a fixed asset investment may be so large that it could lead to the bankruptcy of a firm if the investment fails. Consequently, capital budgeting is a mandatory activity for larger fixed asset proposals. This is less of an issue for smaller investments; in these latter cases, it is better to streamline the capital budgeting process substantially, so that the focus is more on getting the investments made as expeditiously as possible; by doing so, the operations of profit centers are not hindered by the analysis of their fixed asset proposals.

Capital Budgeting Problems

There are several issues with capital budgeting, some of which are caused by the volume and complexity of investment proposals received, and others by the nature of the budgeting process. Two issues arising from large numbers of proposals are:

Project interdependencies. It may be necessary to review how different investment proposals interact with each other. For example, if a proposal to double the capacity of a paint booth is rejected, does this make the investment in a downstream drying room superfluous? Consequently, it may be necessary to first determine the interdependencies of groups of investment proposals, calculate the return on investment for each group, and then decide whether all of the proposals should be accepted.

Conflicting projects. In some organizations, investment proposals are arriving from many departments, without anyone having first reviewed them to see if any of the proposals conflict with each other. For example, one proposal might be to renovate a production line while another proposal is to outsource all production to a third party.

These two issues call for a substantial amount of review time by an analyst who acts as a central coordinator of the capital budgeting process. Two other problems that persistently arise in many budgeting systems are:

Corporate bank concept. The traditional budgeting system has an especially pernicious impact on capital budgeting. The problem is that the budgeting timeline forces most capital budgeting requests to be submitted within a short time period each year, after which additional funds are only grudgingly issued. In effect, this means that the corporate “bank” is only open for business for a month or two every year. Thus, someone may spot an excellent business opportunity for the company, but not be able to take advantage of it for many months, when the “bank” is again open for business. This can be a massive impediment to the continuing growth of a business.

Funding incentive. Given the “bank” issue just noted, managers fight hard for the maximum amount of funding as soon as the “bank” opens – and they spend all of it. But when was the last time that you saw a manager return allocated funds, because he did not feel that the expenditure was needed any longer? That is indeed a rare event! Instead, many managers receive their annual allocation of capital expenditure funds and then push for more funds throughout the budget year for additional projects. In short, the capital budgeting process really creates a minimum funding level, above which a company is very likely to go as the year progresses. It is a rare company that only spends what it initially budgets for fixed assets.

In summary, the budgeting process itself creates two capital budgeting problems. First, it is unusually difficult to obtain funds outside of the budget period, even for deserving projects. And second, managers tend to game the system, so that the capital budgeting process nearly always ends up absorbing more funds than senior management originally intended.

FAQs

How is Risk Considered in Capital Budgeting?

Risk in capital budgeting is considered by analyzing how changes in key assumptions affect a project's outcomes, using tools like sensitivity analysis and scenario analysis. Companies may also adjust the discount rate upward for riskier projects to reflect the higher required return. This helps ensure that only projects with acceptable risk-reward profiles are selected.

Related Articles

Capacity Planning in the Budget